In this week’s wrapup, we look at all the problems plaguing the auto industry and RILs gambit to become net debt-free by 2021.

The Auto Crisis

Maruti Suzuki: Revenue down 15%. Net profit down 28% compared to the 4th quarter last year.

Eicher motors: Revenue down 11%. Profit down 44%.

Hero moto corp: Revenue down 21%.Profit down 15%

Mahindra & Mahindra: Revenue down by 35%. And they made a net loss of 3255 Cr. compared to a profit of Rs.969 Cr.

It’s bad!!!

But these results are symptomatic of a larger trend emerging in the auto industry. A trend characterized by unfavourable market conditions and a general slowdown plaguing the economy.

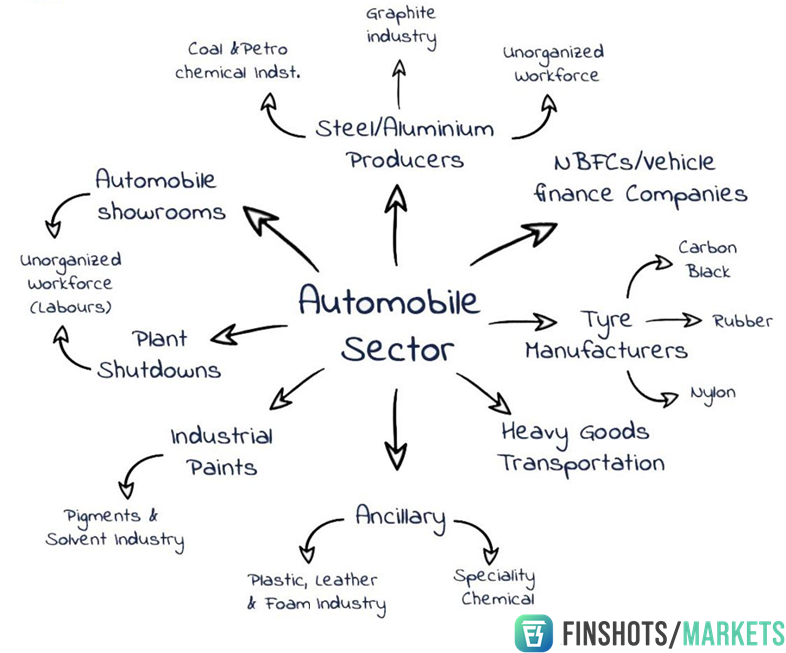

But before we get to the heart of the story, some context. The automobile sector contributes about 7% to the country’s GDP and about 49% to the country’s manufacturing GDP. So if there was a slowdown in the auto sector, the effects wouldn’t be isolated and the contagion would spread quickly. Tyres, Steel, Headlights, Insurance, Leather — components/industries that are closely associated with the auto industry would all suffer in tandem.

However, when signs of a slowdown first began to emerge back in 2018, the incumbents weren’t too concerned. They rationalized the dip in sales by attributing it to a weak festive season. The only problem with this explanation was that there was no convincing argument why the festive season was weak in the first place. The industry association was confident sales would bounce back. But it didn’t.

Then people started blaming the NBFC crisis. After all, the IL&FS debacle was a reckoning moment for the entire industry. Banks were sceptical about lending to Non-Banking Financial Corporations altogether. And since most automobile purchases are financed by the good folks at NBFCs, it is natural for one to presume that the financing crunch would inevitably affect automobile sales.

However, in April 2019, the Reserve Bank of India released a highly technical memo explaining how the NBFC crisis might not have affected auto sales all that much. Instead, they attributed the slump in sales to fuel price and policy decisions — in particular, a change in insurance policies, which increased the upfront cost of purchasing a vehicle.

But the common underlying theme in all these explanations was that this was only a temporary blip and the downturn was unlikely to persist.

But persist it did and policymakers started looking for a new thesis to explain the crisis — “Perhaps the slowdown could be attributed to the proliferation of ride-sharing services and it’s popularity with millennials”, they said.

After all, the likes of Ola and Uber do offer a viable alternative for most commuters. So maybe, ride-sharing did, in fact, put automakers in a quagmire.

However, empirical evidence proved otherwise. The erstwhile memo from the RBI also showed how auto sales took off massively when Ola and Uber started making waves in India.

Think about it. A million drivers were now on board ride-sharing platforms trying to ferry people from point A to point B. It can’t be that all these driver-partners already had vehicles, to begin with, right? Surely many of them were first-timers simply joining the bandwagon because there was so much money to be made. And if that assessment is accurate it can only mean one thing-Ride Sharing helped improve auto sales.

However once the market saturated and there wasn’t as much money to be made plying an Ola/Uber, sales too began to drop. So one could actually argue that we need ride sharing to pick up before we see an uptick in auto sales.

And so, if you can’t attribute the slowdown to anything in particular, why is it happening at all. Well, as 2019 was approaching to a close, India’s growth numbers were stagnating across the board. All the economic indicators were falling in line. This wasn’t just a trend in the auto industry anymore. It was a trend emerging across industries. The auto sector was simply a leading indicator for what was to come and it was finally becoming clear that the Great Slowdown was upon us.

Meanwhile, automakers were reeling from another internal crisis.

In an effort to curb pollution, the Supreme Court had ruled that automakers were to upgrade BS-IV engines to the more environmentally friendly BS-VI variants by April 2020. This decision inevitably forced many companies to invest heavily in changing their production processes in order to accommodate the newer engines.

However, whilst gearing up to produce these swanky new variants their stock of BS-IV vehicles began to pile up. According to industry sources, around 7,00,000 BS-IV two-wheelers, 15,000 passenger vehicles and 12,000 commercial vehicles, all worth around Rs.6,350 crores were lying unsold. And dealers were bearing the full brunt of this burden as they simply couldn’t move this stock quickly enough considering the dip in demand. As a result, many dealers simply shut shop. And with dealers going bust, vehicles began to pile up at the production facilities.

Automakers immediately rushed to contain the damage. They shut down production facilities. Some lasted a week. Some, a fortnight. Layoffs became commonplace and over 3.5 lakh workers lost their jobs. To counter all this, the industry started lobbying to get GST rates down from 28% to 18%. However, with government finances in such terrible shape, that wasn't going to happen either.

And then, the final blow — Coronavirus. With a nationwide lockdown in place, automakers were forced to fully shut down production facilities during the months of April and May. According to the president of SIAM (Society of Indian Automobile Manufacturers), the industry loses ~Rs.2,300 crore, every day their plants remain closed.

Do the math!!!

It shouldn’t surprise you why the auto industry is in such dire straits.

Reliance Industries (RIL) says it’s net debt-free

“Don’t make promises you don’t intend to keep.”

When Mukesh Ambani vouched to turn RIL net debt-free by March 2021, they had a burden of ~Rs 1,54,000 Cr (net-debt). There were a few people who scoffed at this ambitious plan. When the Saudi Aramco deal hit a roadblock, they wrote this idea off altogether. When COVID made landfall, they doubled down on their criticism.

Yet, within 10 months after making the original bet, Mukesh Ambani has seemingly done the impossible. RIL has managed to sell part of Jio Platforms for obscene amounts of money and then they managed to raise more money from existing investors through a Rights Issue.

And not only did Mukesh Ambani keep his promise, but he did it 9 months ahead of schedule.

Also net debt-free status doesn’t mean RIL will have no debt. They will, but they will also have more than enough cash to cover for the debt. Here’s a nice infographic to show how RIL got here.

The Brave new world of Biosimilars

In other news, we were being told Biocon finally had approval from the FDA to market their latest biosimilar — insulin glargine. The problem with this headline is that the pharma industry is devilishly complicated. And to fully decipher what’s happening here, you need a full-blown explainer.

So if you are interested in Biocon or the pharma industry, in general, go ahead and read our piece on biosimilars. We promise you’ll love it.

It’s not you, it’s me — A global agrochemical company terminated a ₹4,000 Cr contract with our very own Aarti Industries after confessing they had a change of heart. The company needed an intermediate chemical compound and Aarti was supposed to manufacture it. So Aarti spent ₹400 Cr putting together a plant to prep this stuff until they were told their services weren’t needed anymore.

Do bear in mind, Aarti can still use the new facility to manufacture other chemicals and they will be entitled to a compensation of about ₹ 900 Cr. So, it’s not all that bad I suppose.

Until next time ...